Foreword

For the past decade, the lithium battery industry has been enveloped in a singular narrative. Demand growth, technological advancement, and scale expansion meant that as long as you moved fast enough, there would always be a place for you. However, by 2025 and beyond, this logic began to break down.

According to McKinsey & Company’s newly released January report, Battery 2035: Building new advantages, the global battery industry stands at a clear inflection point. Demand is still growing, but the “good times” are over; the market is still expanding, but the space for most players is rapidly shrinking. This is not a cyclical fluctuation, but a structural shift.

I. Explosive Demand, But No Profits

In absolute terms, batteries remain one of the most certain growth sectors globally. In 2024, global lithium battery demand exceeded 1 TWh for the first time, is projected to reach 1.6 TWh in 2025, and is expected to be around 4.2 TWh by 2030 and nearly 6.8 TWh by 2035.

The logic behind Electric Vehicles (EV) + Energy Storage Systems (ESS) is clear, but the problem is that supply has expanded too rapidly. By 2025, the global nominal manufacturing capacity for lithium batteries significantly exceeds demand, with actual oversupply approaching 900 GWh. Based on planned capacities, the surplus is even larger. The result is a price collapse. In 2025, the average battery pack price fell to $108/kWh, and cell prices dropped to $74/kWh, halving from 2018 levels.

What does this mean? Combined with McKinsey’s assessment, True Lithium Research believes the battery industry has completed a phased shift from “competing on scale” and has officially entered a new cycle focused on competing on cost, yield rate, and systemic capabilities. At this stage, simply relying on capacity expansion and financing is no longer sustainable. Companies lacking manufacturing advantages will ultimately be cleared out directly by the price mechanism.

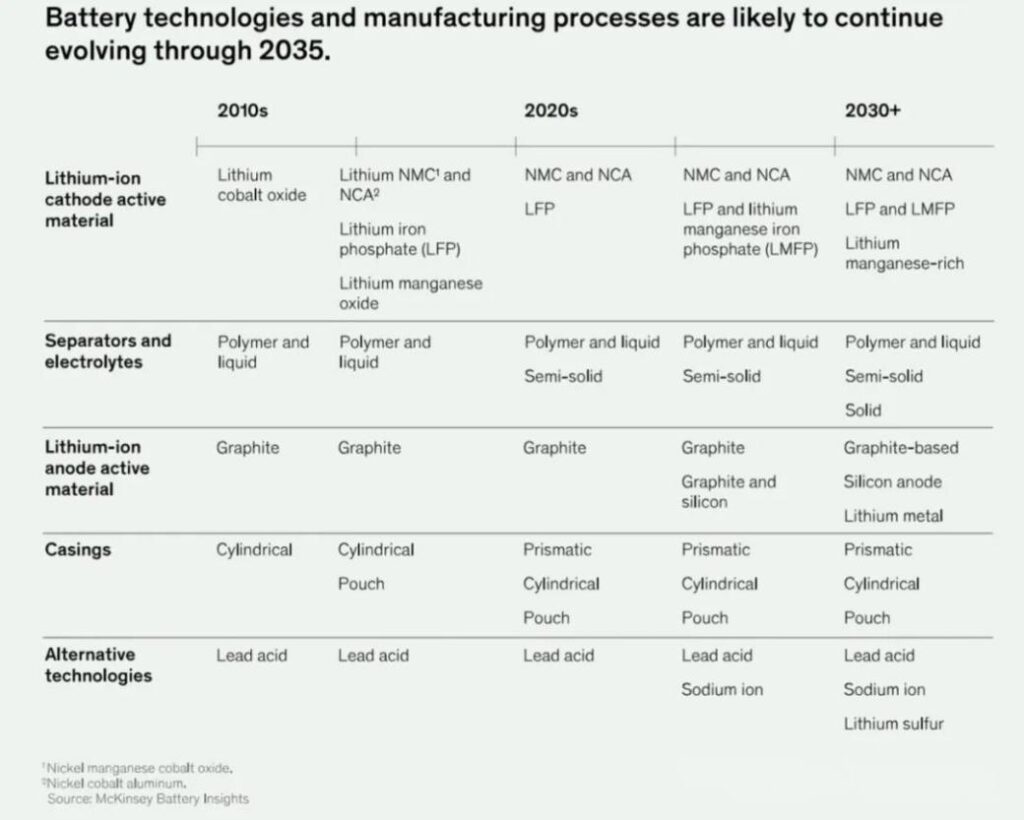

II. No “Revolution” in Technology, Only Continuous Evolution

Many are still waiting for a “disruptive technology,” but McKinsey offers a sober judgment: over the next decade, the mainstream will remain the lithium-ion system, not a sudden generational change.

LFP is the true foundational layer. It has the lowest cost, best thermal stability, and is most suitable for mass-market EVs and ESS. By 2035, LFP’s market share in both Europe and the US is expected to approach 50%. LFP is no longer a “low-end solution” but a fundamental configuration for the global energy system.

NCM exists for performance, but faces increasing pressure. It serves long-range, premium models but carries higher raw material price and geopolitical risks. NCM will not disappear, but it is destined to be a structurally contracting high-end market.

Solid-state batteries are unlikely to become mainstream before 2030. Semi-solid-state batteries can achieve gradual mass production, but full solid-state must overcome three major hurdles: yield rate, cost, and lifespan. By 2030, even if industrialized, solid-state battery costs may remain around $100/kWh, functioning more as a technological reserve rather than a disruptive force.

In summary, the future of lithium batteries resembles “Moore’s Law in the chip industry” more than a generational leap like in mobile phones.

III. The Gap Will Be Determined by Manufacturing Capability

If technology roadmaps are becoming clearer, what determines survival is the manufacturing end. McKinsey repeatedly emphasizes one term: Industrialization Excellence.

Whether a battery factory is profitable hinges on four core aspects:

-

Cost Structure, not betting on raw material price fluctuations. Future battery prices may stabilize but are unlikely to rebound significantly. Cost advantage will come from BOM optimization, energy density improvement, and material usage efficiency. Gambling on lithium prices is no longer viable.

-

Production Line Efficiency. Industry leaders aim for line utilization rates of 80–90%, achieving yield rates of 95%+ within 18 months of operation, and a labor force of 30–40 people per GWh. This represents a set of standards for manufacturing, not a “new energy startup.”

-

Yield Rate is the Biggest Profit Lever. During ramp-up, scrap rates for many battery production lines can be as high as 70–80%. McKinsey’s judgment is direct: reducing one unit of scrap is more profitable than squeezing raw material prices.

-

New Processes are Becoming the New Divide. Dry electrode process, high-speed stacking, digital twins + online inspection. These are not “nice-to-haves” but key variables for the next round of cost curve shifts.

IV. Regionalization Significantly Impacts Costs

In recent years, both Europe and the US have discussed “de-Asianization,” but McKinsey offers a realistic judgment: completely decoupling from Asian supply chains is almost impossible before 2030.

This doesn’t mean Europe and the US will do nothing.

Europe’s problem is clear goals but slow execution. By 2035, it requires €200–300 billion in investment, with severe gaps in raw materials, processing, and midstream capabilities. Project approvals, funding, and technology transfer remain bottlenecks. Europe’s success will depend not on “self-building” but on alliances, joint ventures, and partnerships with global leaders.

The US advantage is funding and aggressive policy. The IRA’s 45X tax credit directly reduces cell costs by 30–50%. ESS demand + AI data centers provide real pull. However, FEOC rules are significantly reshaping supply chain structures. The US has a chance to develop a self-contained domestic battery ecosystem, provided manufacturing capabilities can keep pace with policy incentives.

V. Energy Storage is Critical

An important signal in McKinsey’s report is that Battery Energy Storage Systems (BESS) are transitioning from a “supporting role for renewables” to a “grid necessity.” Global BESS installations are projected at around 200 GWh in 2025, potentially reaching 500–700 GWh by 2030.

Furthermore, the business logic for BESS is entirely different from that of EV batteries. It competes not on ultimate energy density but on system cost, lifespan, operation & maintenance, and revenue structure. LFP will dominate long-term, and sodium-ion batteries have a realistic window in the ESS segment. In Europe and the US, AI data centers + grid constraints + ancillary service markets are pushing BESS to the forefront.

Conclusion

To summarize McKinsey’s underlying assessment in one sentence: the battery industry no longer rewards “stories,” but only “capabilities.”

Companies likely to survive the next decade will generally possess several characteristics: extreme cost control capability; industrialization and yield ramp-up capability; regional compliance and supply chain management capability; and a clear, executable technology roadmap, not a PowerPoint roadmap.

Our industry is at the forefront of its era, but it is no longer an industry where “just being in the right place guarantees survival.” It is returning to the essence of manufacturing—slow, heavy, hard, but real.