If you had told me two weeks ago that a conflict in the Middle East would cause China‘s lithium carbonate futures to hit the daily limit and triple my freight costs for African lithium ore, I might have thought you were exaggerating. But today, standing on the threshold of March 2026, this has become the cost sheet we must face every day.

As a foreign trade professional specializing in drone batteries, I deeply feel that while the flames of war in the Middle East seem distant, they are violently reshaping the global lithium battery industry pattern through three “arteries”: oil, natural gas, and shipping. What we are experiencing is not just short-term market volatility, but a profound rewrite of industrial logic driven by geopolitics.

This article will analyze how this conflict acts as a “stress tester” for the lithium industry from three dimensions: cost transmission, demand reconstruction, and industrial transformation.

1. The “Physical Trauma” of Costs: The Tearing of Energy and Logistics

From late February to early March, with the US and Israel launching military strikes on Iran and the closure of the Strait of Hormuz, the global energy market instantly tightened.

For the upstream lithium industry, this is first and foremost a naked cost shock.

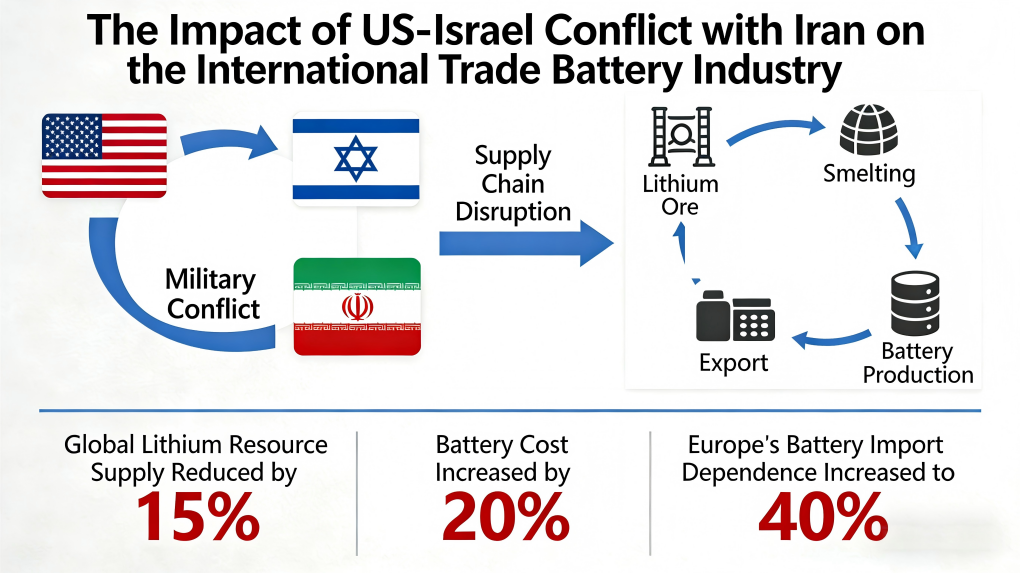

1. Direct Impact of Energy Costs Hard rock lithium extraction is a veritable “high energy consumption” industry. Taking spodumene conversion as an example, the core process requires high-temperature roasting above 1050°C. Producing one ton of lithium carbonate consumes about 1,200 cubic meters of natural gas . When the Middle East situation causes international natural gas prices to spike, and domestic industrial gas prices rise by just 0.5 RMB/cubic meter, it means the cost per ton of lithium carbonate increases directly by 600 RMB. If we factor in the linked costs of coal and electricity, an increase of several thousand RMB per ton is not an exaggeration.

2. Blockage in the “Main Artery” of Logistics The more direct pressure comes from the Red Sea and the Strait of Hormuz. For companies relying on lithium concentrate from Africa, logistics costs have spiraled out of control. Industry data shows that freight rates for African lithium concentrate to China have skyrocketed from around $35 per ton before the crisis to nearly $90 per ton—a nearly threefold increase—with war risk insurance added separately . Shipping times have stretched from the normal 35 days to over 50 days, and the extra half-month at sea means huge capital occupation.

This tearing of costs is rapidly differentiating corporate competitiveness. Companies with their own mines or long-term contract freight rates can still breathe, while small and medium-sized enterprises relying on spot market purchases are caught in the dilemma where “shipping the ore is worse than not shipping it.”

2. The “Internal Injury” of Demand: The Grounding of the Middle East Energy Storage Market

If rising costs are the visible “physical trauma,” then the suppression on the demand side is a more fatal “internal injury.”

Over the past two years, the Middle East has been the most rapidly growing “blue ocean” for global energy storage. Solar and storage projects in the desert, and the new energy blueprint for the Red Sea city, attracted heavy investments from countless Chinese companies like CATL, BYD, and Sungrow. It is estimated that new energy storage installations in the Middle East in 2026 were projected to reach 40 GWh, accounting for about 8% of the global total .

However, the artillery fire of war has disrupted all this.

The closure of the Strait of Hormuz blocks not only oil but also the shipping route to wealth. The market expects that the war will delay energy storage installation progress by 2-3 months, potentially reducing Middle East energy storage demand in 2026 by about 15 GWh . This is a further blow to domestic battery companies already anxious about overcapacity.

On March 3rd, the main lithium carbonate contract on the Guangzhou Futures Exchange hit the daily limit, closing at 150,860 RMB/ton . On the surface, this was a technical correction in the futures market, but the deep-seated reason was market panic over the “collapse of Middle East energy storage demand.” Although in absolute terms, a demand loss of 24,000 tons of LCE (about 1% of total demand) is not enough to destroy the market, in financial markets where confidence is more valuable than gold, it shattered the psychological防线 (defense line) of the bulls.

3. The “Transformation” of the Industry: The Safety Premium and Supply Chain Restructuring

As SMM pointed out, geopolitics is reshaping the energy order: New energy is no longer just a transition narrative, but an asset of national security . This judgment is vividly reflected in the lithium industry.

1. From “Efficiency First” to “Safety First” In the past, we pursued极致 (ultimate) cost and highest efficiency, with globalized supply chains being the optimal solution. But now, war has exposed the fragility of this system. Maritime transport routes, key straits, and supply cuts from a single mine can all become a “Sword of Damocles” hanging over our heads. Consequently, we see two trends:

- Change in Inventory Cycles: Downstream battery and EV manufacturers no longer pursue “zero inventory.” They are starting to build safety stocks and are even willing to share upstream freight costs to secure supply .

- Shift in Technology Pathways: High oil and gas prices make the economics of commercial vehicle electrification increasingly prominent. If logistics fleets perceive a risk of natural gas interruption, they might bypass LNG altogether and accelerate the adoption of electric heavy trucks .

2. The “Matthew Effect” on the Resource Side The divergence in cost pressure is intensifying. The table below clearly illustrates the current situation of different lithium extraction routes:

The market is meticulously calculating each company‘s cost curve. If your mine is overseas, if your energy consumption is high, your profits may be directly scorched by the Middle Eastern flames. Capital is flowing out of high-cost, high-uncertainty assets and into safer havens like salt lake operations or companies with high resource self-sufficiency.

Conclusion

The flames of war in the Middle East act like an extreme stress test, exposing the fragile nodes of the globalized lithium battery supply chain while also highlighting its strategic importance.

In this upheaval, the fates of oil and batteries have become intertwined as never before. Surging energy prices have redrawn the cost curve, blockaded straits have severed demand expectations in key markets, and national security considerations are forcing supply chains to pivot from pure efficiency to resilience. The lithium industry is no longer an isolated industrial track; it has become a crucial piece on the chessboard of great-power rivalry.

Looking ahead, whether the smoke clears or not, the scars left by this conflict will linger: elevated energy costs will be embedded in battery pricing, regionalized supply chains will accelerate, and only those companies capable of navigating geopolitical risks and achieving resource autonomy will truly ride out the cycles. For the entire industry, adapting to this “new normal” may well be the key to breaking through the current predicament.

For more comments like click link: https://www.linkedin.com/pulse/war-oil-batteries-how-middle-east-conflict-reshaping-lithium-amy-wong-eiwwc/

For more analysis about the conflict between USA& Israel and Iran please click link: https://www.linkedin.com/pulse/when-low-tech-changes-rules-war-looking-shahed-136-drone-amy-wong-kklec/?trackingId=ku5LqJYnQUu3WtxOBEf8AA%3D%3D