On May 12, 2026, Shenzhen hosted the 2026 Next-Generation Battery Technology and Industry Development Conference, bringing together leading experts from industry, academia, and research institutions worldwide.

Yet one message from the event surprised many “all-solid-state believers”:

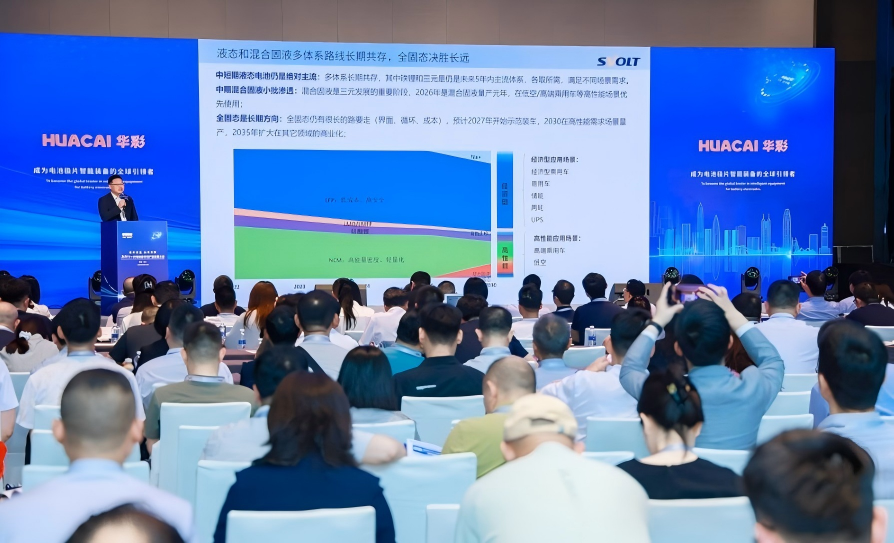

Hybrid solid-liquid batteries are not a transitional technology — they are likely to become a long-term mainstream route. In contrast, all-solid-state batteries may still struggle to achieve cost competitiveness even by 2035.

This statement came from Yang Hongxin, Chairman and CEO of Svolt Energy, and it challenges one of the battery industry’s most widely held assumptions:

“Solid-liquid is only temporary. Once all-solid-state arrives, everything else disappears.”

The conference made one thing clear:

The future battery landscape may not be “liquid → all-solid-state”, but rather “liquid → hybrid solid-liquid → selective all-solid applications.”

Let’s unpack why.

The Dream of All-Solid-State Batteries — And the Distance to Reality

All-solid-state batteries remain the industry’s “ultimate dream.”

Their theoretical advantages are undeniable:

✅ Non-flammable solid electrolytes eliminating thermal runaway risk ✅ Potential energy density exceeding 600 Wh/kg ✅ Wider temperature tolerance ✅ Faster charging potential

China’s industrial white papers already classify the market as entering:

“Hybrid solid-liquid mass production + all-solid pilot verification stage.”

But the conference discussions added significant reality checks.

Technical Barriers Are Larger Than Expected

One major all-solid route today is the sulfide electrolyte pathway.

However, experts pointed out several unresolved issues:

1. Material Stability

Sulfide electrolytes still suffer from:

- Performance degradation

- Moisture sensitivity

- Potential H₂S generation

2. Scaling Problems

Laboratory cells may work.

Scaling from:

- 10Ah prototype cells to

- 60Ah automotive-class cells

introduces major challenges in:

- Cycle life

- Interface stability

- Manufacturing yield

3. Pressure Dependence

Current solid-state systems often require:

≈20 MPa stack pressure

Automakers prefer:

≈5 MPa

This gap remains significant.

Yield Rate: The Hidden Industry Killer

Even if chemistry works, production economics may not.

One painful truth raised during the conference:

A battery that can be built is not necessarily a battery that can be manufactured profitably.

Yield remains a major bottleneck.

Unlike liquid batteries:

10Ah → 60Ah scale-up in solid-state often creates drastic yield drops.

The challenge is not only electrochemistry.

It is manufacturing.

Cost: The Hardest Barrier of All

Perhaps the biggest issue is not performance.

It is cost.

Yang Hongxin stated:

“By 2027, all-solid-state battery material and manufacturing costs may still be several times higher than liquid NCM batteries.”

And remember:

NCM itself remains significantly more expensive than LFP.

This means:

All-solid-state → potentially several multiples above already premium chemistries.

Even 2035 May Not Bring Cost Competitiveness

The conference presented an increasingly common timeline:

2027:

Demonstration vehicle programs begin

2030:

Limited commercialization in premium applications

2035:

Broader expansion begins

Yet even by then:

Cost competitiveness may still remain weak.

Market share could remain limited.

This is perhaps the strongest signal yet that:

All-solid batteries are likely a premium niche before becoming mass-market products.

2026: The First Year of Hybrid Solid-Liquid Commercialization

While all-solid faces long timelines,

hybrid solid-liquid batteries are entering production now.

Yang Hongxin called:

2026 = Hybrid solid-liquid commercialization year.

Target applications include:

✈️ Low-altitude economy / eVTOL 🚗 Premium EVs 🤖 Robotics 🔋 Consumer electronics ⚡ Energy storage

Why Hybrid Solid-Liquid Is Moving Faster

Hybrid systems retain liquid electrolyte advantages:

- Higher ionic conductivity

- Better manufacturability

- Existing production compatibility

While introducing solid components for:

- Safety enhancement

- Higher voltage tolerance

- Better thermal behavior

Result:

Performance improves without rebuilding the entire ecosystem.

Cost Parity Changes Everything

One particularly important announcement:

Svolt plans mass production of hybrid solid-liquid batteries this year.

Their target:

Cost parity with liquid batteries.

Think about that carefully.

If a battery delivers:

✔ Higher safety ✔ Better performance ✔ Similar cost

Why would users refuse it?

This may become the decisive factor.

The Industry Is Already Moving

Several companies showcased hybrid progress:

Gotion High-Tech

Displayed:

- G-Yuan hybrid solid-liquid battery

- Jinshi all-solid battery

The hybrid version was not a concept model.

It was a physical PACK system.

Capabilities reported:

⚡ 9-minute fast charging 🚗 500 km replenishment range 🚗 >1000 km total range 🧠 Predictive safety management

QingTao Energy

Market data indicates:

≈33.6% global share in hybrid + solid-state shipments

≈44.8% share in China

This suggests:

Hybrid systems have already moved beyond laboratories.

Desay Battery

Desay Battery has announced a solid-liquid battery with 420 Wh/kg to be mass-produced by the end of 2026.

Key advantages:

✅ Energy density: 420 Wh/kg

✅ Cycle life: >1,000 cycles

✅ Continuous discharge rate: 20C

✅ Capacity retention at -40°C with 6C discharge: ≥90%

For More details please click below links:

Why This Matters for Low-Altitude Aircraft and UAVs

For people working in drone batteries, eVTOL, and aviation power systems, this shift is even more important.

Low-altitude platforms need:

- Higher energy density

- Extreme safety

- Fast charging

- Lightweight systems

Waiting until 2035 for all-solid batteries is not practical.

Hybrid solid-liquid batteries may become the bridge technology enabling:

✈ Heavy UAVs ✈ Cargo drones ✈ eVTOL aircraft ✈ Robotic aviation systems

before all-solid matures.

Should Consumers Wait for All-Solid-State EVs?

Many readers still ask:

“Should I wait for all-solid batteries before buying an EV?”

After this conference, the answer seems clearer:

Probably not.

Liquid batteries:

- LFP

- NCM

will remain dominant for years.

Hybrid solid-liquid batteries may enter premium vehicles first.

All-solid batteries will likely remain limited initially due to cost.

The battery revolution is happening.

But not exactly the way many expected.

Final Thought

The industry narrative used to be simple:

Liquid batteries → All-solid-state batteries

Now the path looks different:

Liquid → Hybrid Solid-Liquid → Selective All-Solid Applications

Hybrid solid-liquid batteries may not be a temporary compromise.

They may become the long-term mainstream.

And by the time all-solid batteries truly arrive at scale,

the market may already have evolved.

Perhaps the real question is no longer:

“Who wins?”

But:

“Which chemistry fits which application best?”

Because battery history has repeatedly shown:

No single chemistry dominates forever.